Did you know that more than half the population is misinformed about their insurance policies? That’s your perk to unveil, as we're about to decipher the mystery enveloping your everyday insurances.

In today's volatile world, knowing how insurance can be your safety net is crucial. From unexpected natural disasters to everyday accidents, insurance isn’t just a safety measure – it’s a necessity.

The shocking truth is, many people assume having insurance equates to safety – yet the complexity and the exclusions often leave policyholders vulnerable. Did you know that home insurance doesn't automatically cover flood damage? It can be a costly misunderstanding. But that’s not even the wildest part…

Furthermore, car insurance policies widely differ depending on your geographic location and driving record – factors not everyone considers when signing up. Even more surprising is how insurers use big data to predict your risk profile, sometimes leading to unfair premiums. But wait, there’s another layer to this unraveling mystery…

As we navigate through these labyrinthine details of insurance, the nuanced realities might seem daunting. What unfolds next might change your perspective forever. Experienced experts themselves were taken by surprise, as they peeled away at layers of concealed practices that define your policy’s value. Discover what they uncovered…

One of the most baffling aspects is the dreaded “pre-existing condition” clause in health insurance policies. While terms vary, this clause can lead to denied claims, blindsiding countless policyholders who believed they had dependable coverage. The irony is, these pre-existing conditions aren’t always clearly defined, which becomes a loophole for insurers. You’ll find the devil is in the details.

Did you know that life insurance payouts are sometimes contested? If a policyholder partakes in an excluded activity that leads to their demise, families might find the expected safety net falling apart. Understanding which activities are delineated under these exclusions is vital. Yet, many policyholders overlook these details when signing.

This complexity extends to renter’s insurance too. Apart from outright theft, lesser-known specifics like water damage from leaking pipes might not be covered unless explicitly mentioned. Your landlord might be off the hook, leaving you with the bill. Policies often bundle common claims, but the variances can be puzzling!

Endorsing big-name insurance isn't always synonymous with the best coverage. Often, lesser-known insurers offer customized solutions more aligned with individual needs. Navigating through dense policy jargon isn’t easy, but professional advisement can demystify this intimidating task. Still, surprises keep simmering just beneath the surface…

When you think of “full coverage,” your mind likely drifts toward an all-encompassing safety net. What’s important to know, however, is that full coverage for vehicles typically only includes liability, collision, and comprehensive aspects, leaving gaps like roadside assistance or rental reimbursement services. Always demand clarity.

Another neglected aspect is umbrella insurance, designed to fill in those perilous gaps where your primary policies end. Few realize this until it’s too late, often after an unforeseen incident. Unlike regular policies that cap at a certain level, umbrella insurance extends your coverage, but it’s often undersold or misunderstood.

Pet insurance appears straightforward, but hidden clauses can lead to entirely unexpected setbacks. For instance, some policies exclude congenital disorders, leaving pet owners frustrated and financially burdened. Just like people, even furry members need thoughtfully chosen policies that consider all eventualities.

Too often, consumers focus solely on premiums while ignoring deductibles, which might render claims impractical. This misinformation leads to widespread disappointment when claims aren't processed as anticipated. Understanding these crucial elements can significantly influence the true value of a policy, as you’ll see on the next page…

Many employees take comfort in workplace insurance, thinking it’s a secure alternative to individual policies. Yet, most of these plans offer minimal coverage with limitations that aren’t always highlighted. Shockingly, this might leave you underinsured for significant health events, contradicting the perceived safety net.

Are you aware that dental and vision add-ons often involve waiting periods? This unexpected revelation can be a nightmare for those needing immediate services, causing unsuspecting employees to bear the brunt of such waiting times, financially and otherwise.

Furthermore, pensions and annuities can mislead; believing your company has fully secured them without your vigilance might be misplaced trust. It’s prudent to regularly review these benefits and consider external supplementary policies for better financial security upon retirement.

Misunderstood stipulations around coverage for legal consultations also come into play. Many are surprised to learn that involving an attorney for claims disputes can often lead to better resolution but at an additional out-of-pocket expense. The story evolves further with even more intriguing revelations ahead…

While most primarily consider insurance for health and property losses, surprising categories such as wedding or pandemic insurance cover unforeseen societal anomalies. Imagine a once-in-a-lifetime occasion like a wedding being safeguarded against extreme weather, vendor no-shows, or even illness.

Moreover, pandemic insurance was a less-known gem until recent events forced its necessity into the limelight. Companies who had it before COVID-19 hit were undoubtedly thankful, as they faced disruptions with a safety net few had anticipated.

Cyber insurance has also become increasingly valuable as online threats magnify. For businesses, neglecting data integrity can be catastrophic, making cyber policies invaluable. Security breaches are no longer “what-ifs” but "when," prompting insurers to broaden coverage scopes.

The added bonus of professional liability insurance goes unnoticed by many. Whether you’re in finance, law, or healthcare, protecting against potential negligence claims ensures peace of mind. Intriguingly, such innovative insurance solutions continue evolving, each next discovery often more insightful than the last.

Common misconceptions fuel skepticism around insurance; one extensively believed myth is “insurance companies don’t pay out.” While there are unfortunate instances, it's more about misunderstanding policy terms than deceit. Adequate knowledge and patience can often resolve conflicts favorably.

Additionally, there exists a notion that personal items inside cars are automatically insured under auto insurance. Surprisingly, these are usually covered under home or renter’s policies — a realization typically reached too late without careful examination of terms.

There’s also the belief that older individuals pay more for life insurance. While age is a factor, insurers consider overall health, lifestyle, and hobbies in underwriting, demonstrating that older adults in good health might receive better rates than younger high-risk individuals.

Notably, canceling a policy can seem like ending all liabilities, yet certain penalties may apply. Understand every clause to avoid amplified fees and ensure decisions align with your financial strategy. As we transition to a deeper understanding, yet more revelations lie ahead.

Insurance has evolved from traditional packages to customizable policies, allowing you to tailor coverage to perfectly fit personal needs and budget constraints. This flexibility is a boon for those with unique lifestyle requirements or fluctuating income patterns.

Imagine a scenario where you pay for car insurance only when you drive or augment health coverage based on ailment risk factors. Behavioral data fuels this innovation, rewarding careful drivers or healthy individuals with favorable policies.

These tailored policies open doors for innovative coverage solutions, from pay-per-mile auto insurance to specific ailment-related health insurance. Importantly, customization can potentially lower costs without compromising essential security.

However, as convenient as this sounds, ensuring you have a comprehensive understanding of what’s included versus excluded is paramount. Overlooking minutiae can convert a presumed safety net into a financial sinkhole if gaps go unnoticed. Stay tuned for even more compelling insights!

Technology has revolutionized the insurance landscape; AI and IoT have empowered policies with unmatched accuracy and efficiency. Today, random home inspections or vehicle damage assessments can be done remotely, expediting claim processes significantly.

Innovative use of wearables provides real-time data, enhancing health insurance accuracy and personalized plans. These wearables track vitals, encouraging healthier lifestyles while reducing premiums — all thanks to sustained good health indicators.

Telematics in vehicles represents another frontier, meticulously tracing driving patterns and habits to offer risk-adjusted auto insurance. Safe driving is increasingly rewarded with reduced premiums, a compelling paradigm shift driven purely by tech innovation.

While tech-driven solutions promise unparalleled convenience, the challenge of balancing data privacy cannot be ignored. A wary eye on data security as these technologies expand is necessary to prevent misuse. We’re just past the surface of this transformation; deeper understanding is just ahead.

While premiums and deductibles dominate most insurance discussions, sundry often-overlooked expenses collectively inflate actual insurance costs. Administrative fees, policy changes, and late fees subtly add to overall expenditure.

Consumers frequently find their policies riddled with add-ons, from roadside assistance to extended warranties, designed to convenience with little explanation on their long-term costs. Regular comparisons are crucial in ensuring you aren’t overpaying.

Scope creep can further escalate costs. Policy extensions or amendments without thorough scrutiny may include unnecessary coverage. Being proactive in auditing these aspects regularly can help identify potential savings.

Lastly, educating oneself on jargon like “coinsurance” and “co-pay” is pivotal, given their significant influence on out-of-pocket expenses. Emerging insights from subsequent pages will continue to clarify these intricacies, placing you in a better decision-making position.

While many opt for self-service software to streamline policy searches, complex insurance needs often justify enlisting a professional agent’s expertise. Agents decode legal jargon and secure optimal contracts that DIY methods might overlook.

Agents also provide crucial insights on long-term cost efficiencies, evaluating life changes that might impact coverage needs. From upgrading homes thereby increasing home insurance, to adjusting life insurance based on family dynamics, their guidance is indispensable.

Comparing insurance agents is akin to evaluating different policies themselves; their approach, experience, and integrity directly influence decisions and outcomes, demanding careful consideration before selection.

Should you divulge new information such as changes in health or occupation, an agent reassesses and adjusts policies accordingly, thereby safeguarding your interests. Enriched by these proficiencies, your insurance strategy can thrive — but the story doesn’t end here…

Travel insurance has transitioned from a mere luxury to a necessity, especially in today’s post-pandemic era of uncertainties. Beyond ticket cancellations and lost luggage, policies now encompass unforeseen medical emergencies abroad, providing crucial peace of mind.

The introduction of biosecure travel insurance offers coverage for scenarios such as enforced quarantines or trip cancellations due to health guidelines, addressing contemporary traveler anxieties.

Admittedly, understanding the fine print can be taxing; many travelers remain unaware of exclusion clauses within geographic zones or specific activities undertaken abroad. Misunderstanding these elements risks unexpected out-of-pocket expenses.

Thus, it’s paramount to select policies aligned with your itinerary; e.g., high-risk adventure trips might necessitate specialized coverage. Armed with tailored knowledge, venturing out becomes less daunting, underpinned by a robust safety net. The heart of these policies is further explored as we continue.

Insurance policies often confound policyholders with esoteric language and dense terminology designed to obfuscate rather than illuminate. Decoding this language is imperative for understanding coverage and ensuring the policy aligns with personal necessities.

Most recognize terms like “premium” and “deductible,” but subtleties such as “endowment” or “rider” can potentially overwhelm. These misunderstandings facilitate undue reliance on assumptions, which can prove costly in claims processing.

Unpacking these terms not only nurtures better comprehension but aids in leveraging policies ideally suited to individual needs. Agents’ expertise often becomes invaluable in clarifying these complexities, thus steering financial decisions effectively.

Unlocking this language can result in better negotiation leverage. Empowered with knowledge, policyholders can rightfully challenge extortionary terms and enhance their standing against formidable insurance enterprises. Stay tuned, profound revelations await your ensuing clicks.

Crafting an insurance portfolio isn’t exclusively for agents or financial advisors; with accessibility to resources and knowledge, individuals can build bespoke portfolios tailored to specific needs and life goals.

Begin by identifying essentials—health, life, property, etc. Incorporate personal financial objectives like savings, and align these with corresponding insurance solutions. Incorporate adjustments reflective of your life stages.

DIY portfolio management isn’t without hurdles; critical evaluation of potential risks and regular review cycles inform necessary adjustments and refinements, ensuring continued relevance through life’s unpredictable pathways.

Ultimately, a well-crafted portfolio can foster financial resilience, mitigate risk exposure, and secure greater peace of mind should uncertainties manifest. Learn through integrative insights as we delve further into this comprehensive subject.

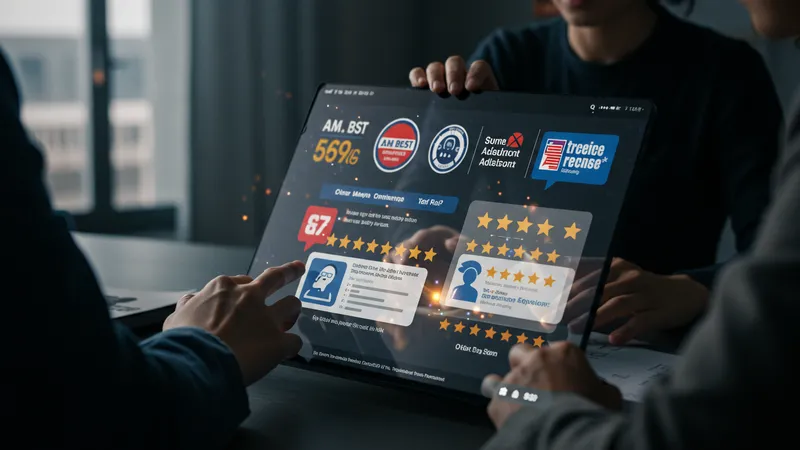

Online reviews have gained prominence, influenced profoundly by real customer experiences. But caution is warranted; assessments can reflect specific viewpoints rather than a comprehensive perspective on an insurer’s effectiveness.

Additionally, independent rating agencies like A.M. Best or Moody's provide neutral assessments of financial soundness, crucial for evaluating insurers’ solvency and reputation. Discovering an insurer’s rating can significantly impact decision-making processes.

Consumer reports often detail additional factors like customer service quality, claim responsiveness, and premium adaptation, helping to distinguish firms offering genuine value from those purporting hollow promises.

While assorted ascriptions to reviews exist, a multifaceted evaluation—reviews, ratings, financial health—results in a multifaceted understanding, enriching subsequent insurance decisions. As the story unfolds further, each aspect interlocks in the complexities of insurance.

The insurance industry isn’t immune to evolving market dynamics: sustainability initiatives express insurers’ commitment to addressing climate impact by offering green insurance products with incentives included.

AI advancements peg insurer predictions as more accurate, thereby reducing premium disparity and driving efficiency. Accordingly, this tech-fueled advancement promises unmatched customer-centric solutions, transforming policyholder experiences radically.

Predictive analytics and genomic data increasingly redefine life insurance policies. By anticipating potential health changes, insurers customize offerings based on personal risk profiles, influencing traditional models.

But technological dependence invites ethical scrutiny; balancing intrusive diligence with personal privacy is paramount. These forward-thinking shifts herald a new era, where innovation aligns with dynamic consumer needs. Await pivotal insights as you continue reading.

As innovations redefine insurance landscapes, positioning oneself amidst these evolutions becomes ever more significant. Prepare by staying informed, ensuring adaptability to new insurance paradigms becomes feasible smoothly.

Engage actively with both industry updates and consumer trends. Participation at seminars or subscribing to forums ensures you remain informed about movement within this evolving sector, both proactive and reactive measures becoming second nature.

An understanding of evolving concepts like microinsurance—catering to specific underserved segments—brings insurance accessibility to broader demographics, presenting novel opportunities for comprehensive coverage.

The narrative concludes by anchoring ambition with foresight, revealing techniques to protect against future risks constructively. Empowered with knowledge, strategy formulation becomes a well-informed journey. Continue for your final dose of indispensable insight.

The tale of insurance is a convoluted one, layered with complexities and intrigue, yet armed with the right insights, navigating this labyrinth is an opportunity for empowerment. Whether customizing portfolios or embracing tech reforms, the insurance landscape teems with potential waiting to be harnessed. So, why keep this knowledge to yourself? Share this article, bookmark the insights, and transform your approach to insurance forever.